Still, an already volatile fixed income environment could get even more so as central banks worldwide chart their own policy paths. We survey the fixed income landscape and identify where we think attractive opportunities can be found. Frédérique Carrier writes

Elevated bond yields have rekindled investor interest in fixed income, given the battle against inflation is making pleasant progress in many regions and most central banks in advanced economies are nearing the end of their rate hiking cycles. But Japan moving away from its super-loose monetary policy could add to an already volatile backdrop. We continue to see opportunities in emerging market fixed income, where the rate cutting cycle has kicked off in earnest.

Go deeper with GlobalData

Inflation progress to continue?

Inflation has pleasingly receded in most regions. In the U.S. it declined to 3.2 percent year over year in July, while in Canada it was down to 2.8 percent in June. European inflation also slowed in June, though to a still higher level of 5.3 percent. Even UK inflation—stubbornly high for most of the year—retreated to 7.9 percent in June, the lowest level in 15 months.

However, these improvements should not be taken for granted. Higher oil and food prices and fast wage growth could slow the recent progress.

Oil prices surged over the past month, with West Texas Intermediate crude oil shooting up to more than $84 per barrel from less than $70 per barrel a month ago. This, in turn, is feeding upward pressure on gas prices.

Food prices could also spike. The summer’s intense global heat wave could undermine harvests across at least three continents, while the Russia-Ukraine war is disrupting Ukrainian grain shipments through the Black Sea and risks further damaging supply chains.

How well do you really know your competitors?

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Thank you!

Your download email will arrive shortly

Not ready to buy yet? Download a free sample

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

By GlobalDataWage-price spirals are another key upside inflation risk. According to the Atlanta Fed’s wage growth tracker, the actual rate of wage growth in the U.S. currently remains brisk and has slowed only modestly, to six percent year over year from a peak of 7.1 percent last year. In the UK, wage growth exceeded seven percent year over year in May.

For central banks, wage growth will continue to be a key factor to monitor, though we think many will likely look past food/energy inflation. For now, most countries are celebrating the progress they’ve made in controlling inflation.

Japan is the exception. As it reopened its economy in late 2021 after strict COVID-19 lockdowns, inflation crept in, reaching a high of 4.3 percent in January 2023. The Bank of Japan (BoJ) was initially very tolerant of higher inflation as a tool to revive long-term inflation expectations, setting its policy on a different course than that of its developed nation peers.

Nearing the end of the hiking cycle

Central banks in the U.S., Canada, the UK, and Europe are at or nearing the peaks of their hiking cycles.

With the Fed having raised the upper end of the fed funds rate target range to 5.50 percent in July, markets believe Fed rate hikes are now likely in the rearview mirror. We concur, as we expect the Consumer Price Index and jobs report that are scheduled for release before the Fed’s next policy decision on September 20 to show that things are moving in the right direction. The Fed, in our view, may well be ready to end its tightening cycle by then.

The Bank of Canada (BoC), the European Central Bank (ECB), and the Bank of England (BoE) all raised interest rates by 25 basis points (bps) in July, to five percent, 3.75 percent, and 5.25 percent, respectively, and adopted a highly data-dependent approach. We think that may mean the BoC and ECB will take no action at their next policy meetings in September and remain on hold henceforth. The BoE remains the outlier, and markets expect two more hikes which would bring the peak rate to 5.75 percent.

Unwinding super-accommodative policy

The BoJ stepping away from its ultraloose monetary policy is a relevant development that investors shouldn’t overlook. As a result of this policy, the BoJ has been injecting cash into the global financial system. Withdrawing this liquidity could potentially amplify the volatile backdrop in fixed income markets.

The BoJ’s so-called yield curve control policy—put in place seven years ago to fend off deflationary risks—requires the central bank to buy benchmark 10-year Japanese government bonds (JGBs) in an effort to hold down their yields.

As inflation returned to Japan, the yield curve control policy was first relaxed in December 2022 when the BoJ increased the yield ceiling to 0.5 percent from the previous 0.25 percent limit. In July, with the most recent reading of core inflation (excluding fresh food and energy prices) reaching 4.3 percent year over year, it extended the ceiling further to one percent. As a result, the 10-year JGB yield surged to over 0.60 percent at one point—the highest level in nine years.

Cutting policy rates

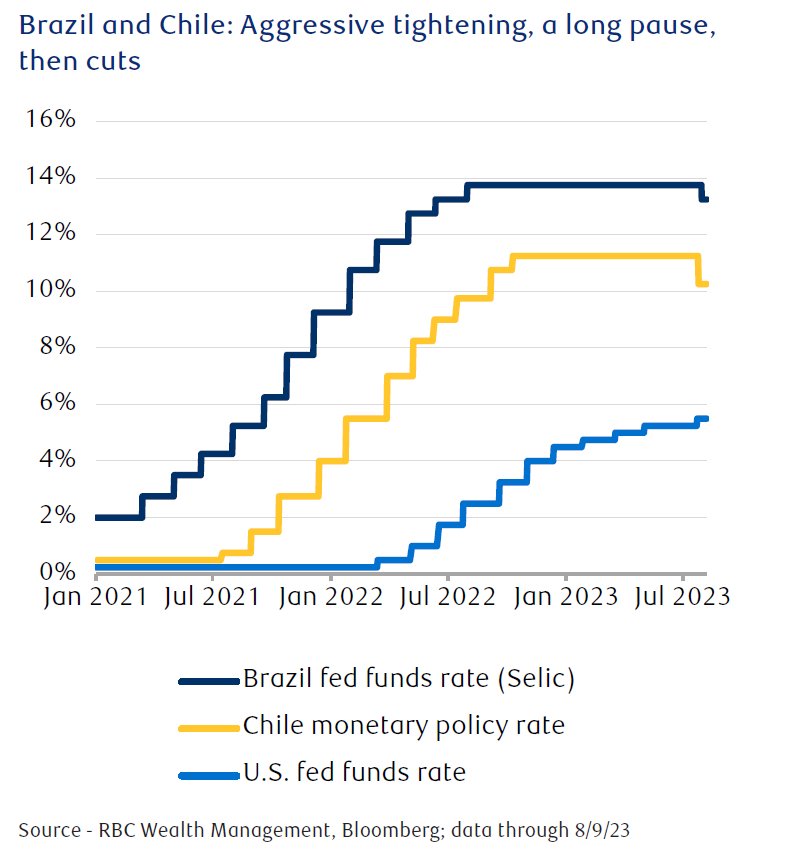

By contrast, in emerging markets the rate cutting cycle is well underway. Two central banks in Latin America are aggressively lowering rates—this has caught our eye as we’ve been highlighting emerging market fixed income as an attractive opportunity for investors.

Central banks in Brazil and Chile hiked early—in the case of Brazil, a year before the Fed—and aggressively due to the greater sensitivity of their economies to food prices and capital flows. Moreover, lacking the Fed’s reputation for fighting inflation, they set out to prove their credentials. This was particularly important to the Central Bank of Brazil, which only became independent in 2021. With inflation declining to just over three percent year over year, in line with its target, from a peak of 12 percent in April 2022, Brazil cut interest rates by 50 bps in early August. This followed in the footsteps of Chile, which cut rates by 100 bps in July.

We look for other emerging market central banks that also have taken preemptive action on inflation to cut rates over the next few months.

Windows of opportunity

Bond markets have been very volatile so far in August, with the 30-year U.S. Treasury yield experiencing one of its most rapid increases of the past year. The rise was due to a combination of U.S. economic strength and fading inflation that could allow the Fed to be less aggressive, paving the way for a longer economic expansion. But we think the divergent paths that central banks are setting out on may also contribute to a volatile backdrop.

In our view, such volatility can provide interesting entry points for investors who can now put money to work at yields that have eluded them for much of the past decade. We think emerging market fixed income remains an attractive opportunity for investors as monetary policy is gradually being relaxed, though being selective is of prime importance.

Frédérique Carrier is the head of investment strategy for RBC Wealth Management in the British Isles and Asia

Related Company Profiles

RBC Wealth Management